Last updated on

5 bad loans have been sold on 14 June 2018. They had experienced serious problems of payment and reached more than 120 days delay. This is the second time such operation is performed. Since the beginning of Klear, 8 loans have been sold among the 580 we have financed.

These 5 loans were purchased by Klear at 34.7% of their value.

Why purchased by Klear?

Because the highest price we received from debt collection agencies was below 30% and we considered that it was not enough. So, we decided to purchase and to match the price obtained during the first debt sale.

The total amount due of these 5 loans was 48 594 BGN. They have been purchased at 16 862 BGN, i.e. with a discount of 65.3%.

What are the impacts?

The impacts are pretty much like the ones from the first debt sale.

Nothing unexpected. Losses from bad debt are considered in the P2P model. Part of all the interest paid by the loans performing well is dedicated to cover such losses.

In this article, we’ll show how the profit and the yearly return have been impacted. In a second part, we wrap up the key takeaways from this second debt sale. In the last part, we give some hints about the next steps. If you already experienced the first debt sale, you can skip the second and third parts as the conclusions are the same.

1. Impacts

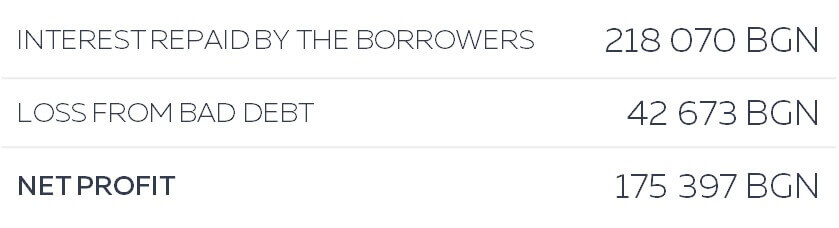

Profit on the whole Klear portfolio

As we can see, the total amount of interest paid by all the borrowers exceeds by far the loss coming from the sale of these non-performing loans.

Yearly return in % of the whole portfolio

The Average Yearly Return of the whole portfolio logically falls from 7.1% to 6.2%, remaining above the forecasted 5.5%.

Dispersion of the impacts and factors influencing them

After the debt sale, the yearly return per investor varies from –18.94% to 128.56%, with an average of 7.0%. The graph below shows the distribution of the yearly returns.

The dispersion of the returns comes from 2 main reasons, the activity on the secondary market and the number of loans.

Below are 2 graphs representing the yearly return by average number of loans. The first graph relates to investors having transacted on primary and secondary markets, the second to investors having only transacted on the primary market.

As we can see, the dispersion is higher on the first graph. Some investors have an abnormal low return because they purchased at a discount lower than 65.3% one of these bad credits, which means that they ended up with a negative balance on this operation.

The dispersion on the second graph (investors not having transacted on the secondary market) is way narrower and none of them has a negative return.

Besides, we can notice that when the number of loans increases, the dispersion of the yearly return is lower. It proves that investing in many loans (high diversification) reduces the volatility.

2. Key takeaways

Key takeaway 1

If you decide to buy on the secondary market, do not overpay for a loan in trouble. Check that the discount proposed by the seller is close to the KIP of the loan.

If you decide to liquidate your portfolio, don’t sell it below its value. Sell loans which are OK (KIP =0) without discount and the others with a discount close to KIP.

If you notice loans in delay in your portfolio, don’t panic. It’s normal. That’s part of the model. There is no need to sell them.

Key takeaway 2

Investing in more than 150 loans, only in the primary market, is the best strategy to ensure a return close to the expected average.

3. What’s going to happen next after this second debt sale?

On the whole portfolio

We’ll continue to sell portfolios of loans reaching more than 120 days.

After some time, the average yearly return will progressively converge towards the forecasted value, around 5.5%.

For each investor

With time, if you keep reinvesting in loans, the return should converge progressively to a value close to the average forecasted.

This will happen if the diversification level is high. We recommend each investor to set up a strategy to achieve a level of 150 loans in a maximum of 3 months.

---

Want to understand more about the calculation of the yearly return and its evolution? Read this FAQ.

We carried out our first debt sale

We carried out our first debt sale

Results after 1 year of investing with Klear

Results after 1 year of investing with Klear