1 year after Klear P2P investing platform launched, what are the actual results compared to the promises made?

They are good!

Here are the numbers.

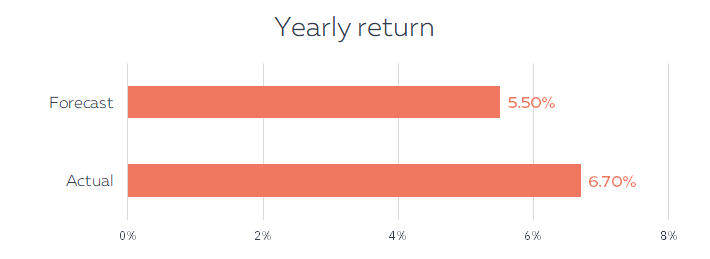

1. The average yearly return stands at 6.7% vs 5.5% forecasted

This is fine, no surprise.

It’s also logical to have an actual return still above the forecast because the portfolio is rather young.

Therefore, we keep our midterm forecast of 5.5% average yearly return.

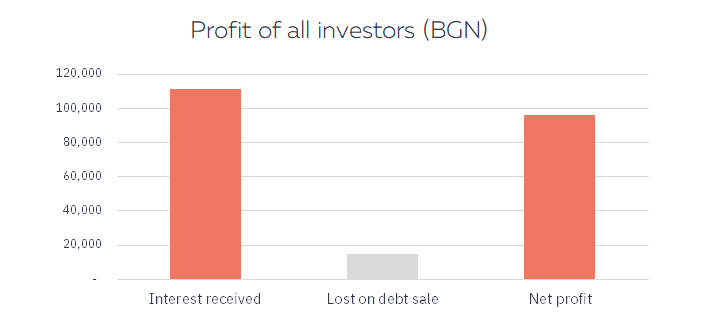

2. The net profit of all investors has reached 100K BGN

Here also it’s fine.

Yes, some borrowers are not paying. Unfortunately, accidents of life happen. But it is statistically considered when designing the product. Part of the interest paid by the borrowers is there to cover the loss from these very few non-performing loans.

This is a clear illustration that the P2P model works.

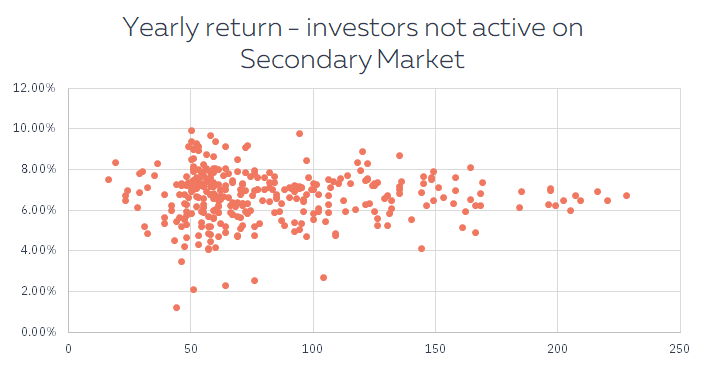

3. Investors with the highest diversification have the most stable returns

This is the return of each investor who did not transact on the secondary market, depending on the average number of loans he has invested in.

It clearly shows that the deviation from the average return is smaller when the number of loans is high.

Investors purchasing on the secondary market (this is the place where loans with problems are sold) have more volatile returns. It’s why we do not recommend going there before being very experienced.

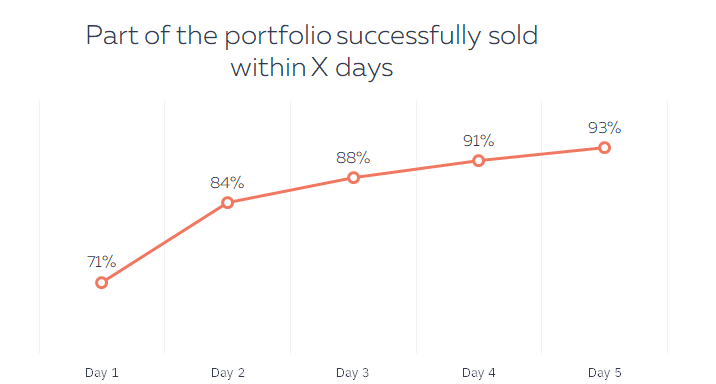

4. If an investor wants to sell its portfolio, it goes rather fast

93% of the total amount of parts of loans listed for sale were sold within 5 days.

Understandably, smaller amounts are going faster than bigger but, on average, it is fast.

It also takes longer for the small shares of loans in delay as there is less appetite from potential buyers. At worst, they will be purchased – with discount - in case they do not pay and end up being sold to an external debt collection agency.

5. Klear filters drastically. Only 10% of all credit applicants are approved

All applicants and their spouse are checked in the Central Credit Register. None with current delay is accepted.

The National Social Security Institute (NOI) is systematically consulted to assess the incomes of the household. Sometimes, it’s also the Trade Register.

The Household budget and its stability in the future are thoroughly analyzed.

Besides, Klear is using advanced credit scoring algorithms to predict potential defaults.

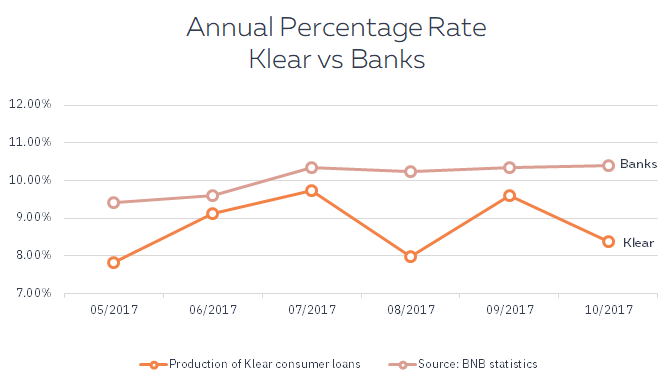

6. Klear is competing with banks, lending to good profiles

Pricing is the secret sauce.

Klear is the first non-bank providing personal loans on average cheaper than banks.

No payday loans. No expensive fast small loans.

Beyond the convenience of the process, offering these excellent conditions is key to attract borrowers with a stable situation and a perfect credit history.

We carried out our first debt sale

We carried out our first debt sale

TOP 10 Everything about Peer to Peer Lending

TOP 10 Everything about Peer to Peer Lending

Klear launches Auto Invest

Klear launches Auto Invest

5 ways to invest with Klear

5 ways to invest with Klear